Does Highmark Cover Custodial Care Services?

Navigating the complexities of insurance coverage for custodial care can feel like navigating a labyrinth. Many individuals seeking long-term care solutions find themselves asking, “Does Highmark Cover Custodial Care Services?” This article aims to shed light on this specific question, providing clarity and guidance on this often confusing topic.

Understanding Custodial Care and Its Importance

Before delving into Highmark’s coverage, it’s essential to have a firm grasp of what custodial care entails. Custodial care focuses on assisting individuals with activities of daily living (ADLs), such as:

- Bathing and Dressing: Helping individuals with personal hygiene and getting dressed.

- Toileting: Providing assistance with using the bathroom and maintaining continence.

- Eating: Preparing meals and assisting with feeding if necessary.

- Mobility: Helping individuals move around their homes safely, including transferring from bed to a chair.

- Medication Reminders: Reminding individuals to take medications as prescribed.

Highmark Custodial Care Needs

Highmark Custodial Care Needs

Custodial care is not medical in nature; it doesn’t involve skilled nursing procedures. It’s about providing hands-on assistance to maintain an individual’s quality of life and independence as much as possible.

Highmark’s Stance on Custodial Care Coverage

Generally, Highmark health insurance plans do not cover custodial care services. This is because most health insurance policies, including Highmark, primarily focus on covering medically necessary services and treatments. Since custodial care is not considered a medical treatment, it typically falls outside the scope of standard health insurance coverage.

However, there are exceptions to this rule. Certain Highmark plans, such as long-term care insurance policies, might offer coverage for custodial care. These plans are designed specifically to address the needs of individuals requiring extended care, including assistance with ADLs.

Highmark Long-Term Care Policy Document

Highmark Long-Term Care Policy Document

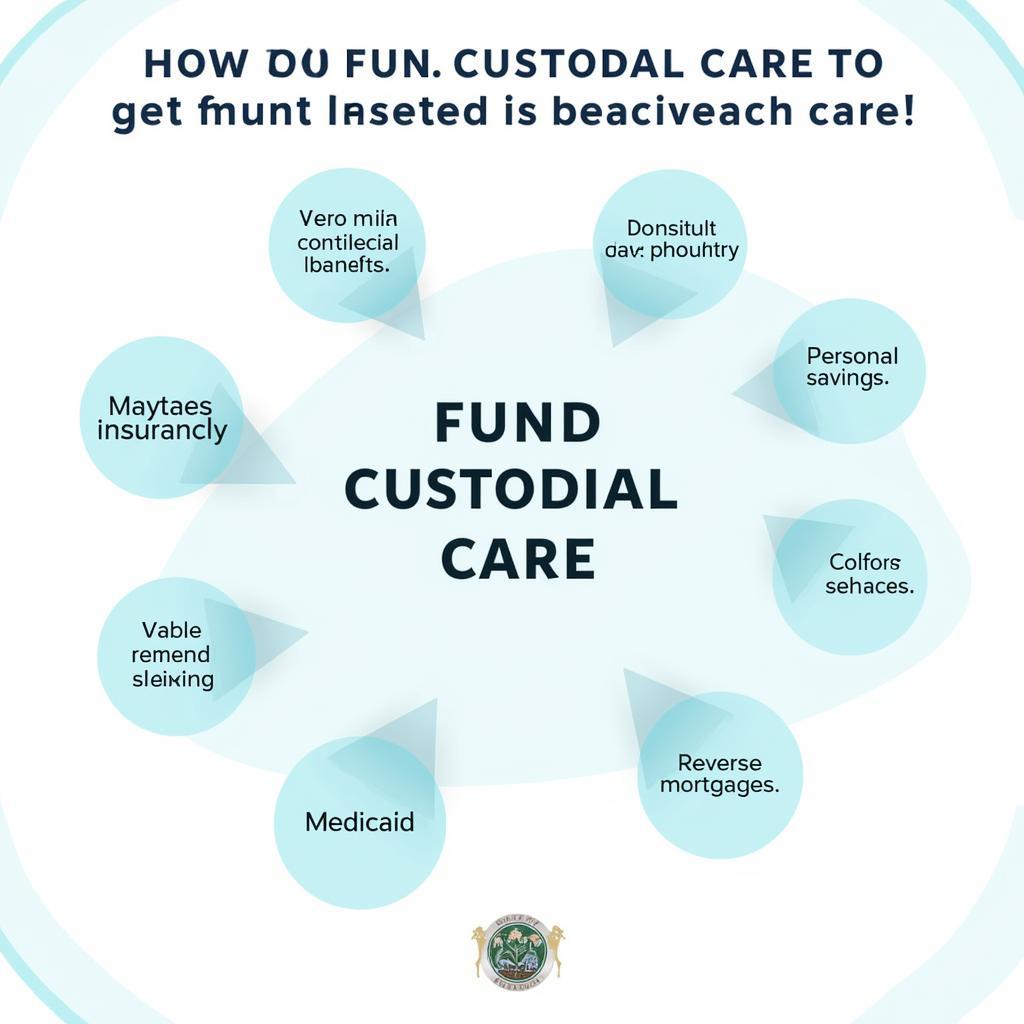

Exploring Alternatives for Custodial Care Funding

If you or a loved one require custodial care and Highmark health insurance doesn’t cover it, don’t despair. Several alternative avenues can help fund these crucial services:

- Long-Term Care Insurance: As mentioned earlier, these specialized policies can cover custodial care costs. It’s best to inquire about Highmark’s long-term care insurance options and their specific coverage details.

- Medicaid: In certain situations, Medicaid may provide financial assistance for custodial care, but eligibility criteria and coverage limits vary by state. Consulting with a Medicaid specialist is recommended.

- Personal Savings: Utilizing personal savings or assets is another option, though it can be financially straining.

- Reverse Mortgages: For eligible homeowners, reverse mortgages can tap into home equity to fund long-term care needs, including custodial care.

- Veterans Benefits: Veterans might be eligible for benefits that cover some custodial care expenses. Contacting the Department of Veterans Affairs for information is advisable.

Exploring Funding Options for Custodial Care

Exploring Funding Options for Custodial Care

Speak to a Highmark Representative

Navigating the insurance landscape can be challenging. If you’re unsure about your specific Highmark plan’s coverage for custodial care, don’t hesitate to contact Highmark directly. Their representatives can provide personalized guidance based on your policy details and circumstances.

Conclusion

While standard Highmark health insurance plans typically do not cover custodial care, options like long-term care insurance policies might offer coverage. Remember to thoroughly review your policy documents or contact Highmark directly for clarification. If your current plan doesn’t cover custodial care, explore alternative funding avenues to ensure you or your loved one receive the necessary support.