Understanding how your primary insurance calculates costs for fee-for-service medical care can save you money and prevent unexpected expenses. Fee-for-service plans differ from other healthcare models like HMOs or PPOs, and understanding these differences is crucial for managing your healthcare budget.

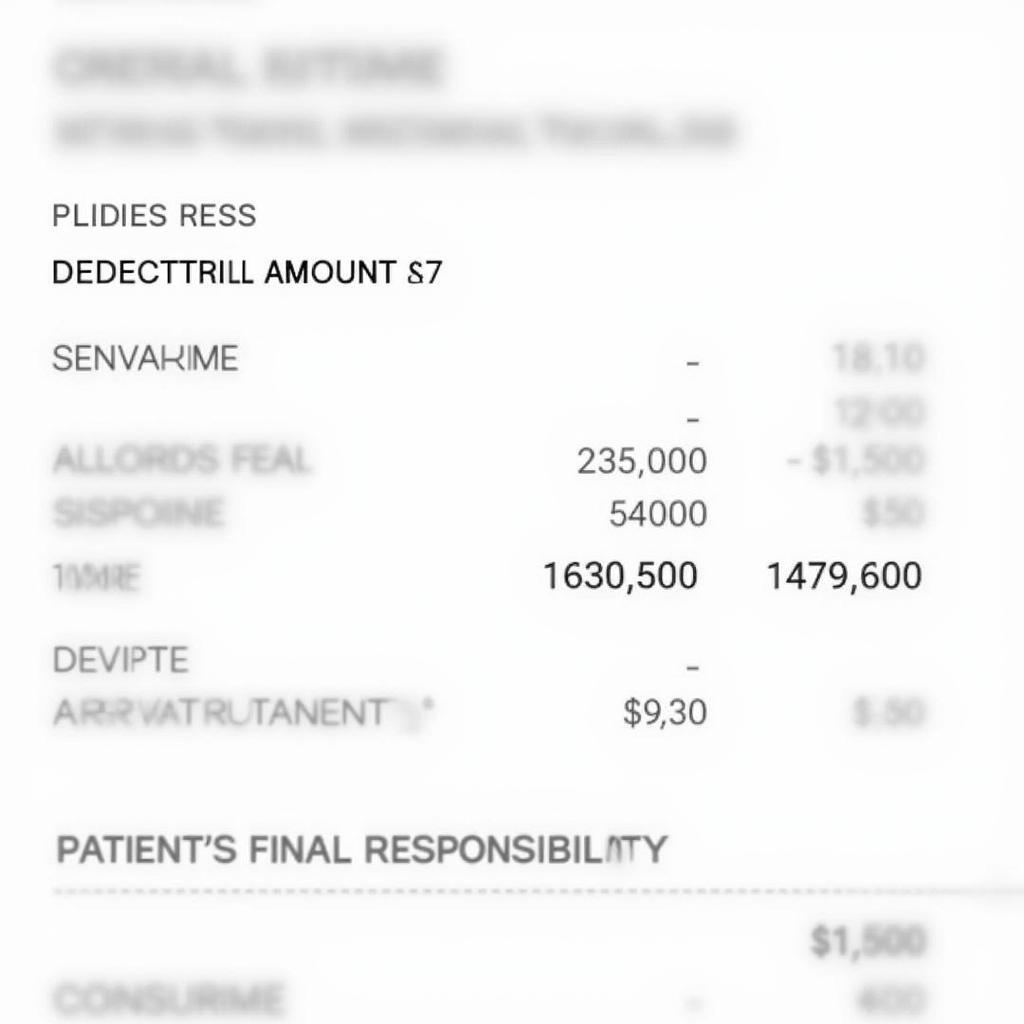

When you have fee-for-service medical care and use your primary insurance, your insurance provider negotiates a discounted rate for various medical services with doctors and hospitals within their network. This discounted rate is often referred to as the “allowed amount.”

Deciphing Your Fee-for-Service Coverage

Here’s a step-by-step breakdown of how primary insurance calculation typically works for fee-for-service medical care:

- You Receive Medical Service: You visit a doctor or healthcare provider within your insurance network for a specific service.

- Provider Sets the Fee: The provider determines the cost of the service and sends a claim to your insurance company.

- Insurance Negotiates Allowed Amount: Your insurance company reviews the claim and determines the “allowed amount” they’ll cover based on your plan’s benefits.

- Deductible & Coinsurance: Depending on your plan, you may have to pay a deductible – a set amount you pay for healthcare services before your insurance kicks in. After meeting your deductible, you may be responsible for a percentage of the remaining costs, known as coinsurance.

- Your Out-of-Pocket Payment: You pay your portion of the costs, which includes any deductible, coinsurance, or copayments.

- Insurance Pays the Rest: Your insurance company covers the remaining portion of the “allowed amount.”

Factors Influencing Your Costs

Several factors can influence the final cost you pay for fee-for-service medical care:

- In-Network vs. Out-of-Network Providers: Utilizing healthcare providers outside of your insurance network can significantly increase your out-of-pocket expenses. Always check if a provider is in-network before scheduling an appointment.

- Type of Service: The complexity and type of medical service required will impact the cost.

- Your Specific Plan: Every insurance plan is unique. Carefully review your plan documents or contact your insurance provider to understand your specific coverage details, deductible, coinsurance percentages, and out-of-pocket maximums.

Navigating Fee-for-Service Medical Care

Fee-for-service plans provide flexibility in choosing your healthcare providers. However, they require a clear understanding of your coverage and proactive management of costs. Here are some tips:

- Stay In-Network: Whenever possible, choose healthcare providers within your insurance network to maximize your coverage and minimize out-of-pocket costs.

- Understand Your Benefits: Familiarize yourself with your plan’s deductible, coinsurance, and out-of-pocket maximum.

- Don’t Hesitate to Ask Questions: If you have any uncertainties about your coverage or a medical bill, reach out to your insurance provider for clarification.

By understanding how primary insurance is calculated for fee-for-service medical care, you can make informed decisions about your healthcare and manage your expenses effectively.